Thus, the amount of interest you pay for the very first payment is $100 [$ 100 = 10%/ 12 months * $12,000). As a result, with the very first payment, you will pay for your principal by $154. 96 [$ 154. 96 = $254. 96 $100] For the 2nd month's payment, you will pay a somewhat smaller sized interest charge, due to the fact that the very first month's payment will have paid down the principal by $154. 96. So, the second payment will include $98. 71 of interest charge [$ 98. 71 = (10%/ 12 months) * ($ 12,000 $154. 96)], and will pay down the principal by $156. 26 [$ 156. 26 = $254. 96 $98.

In this way, as you pay for a vehicle loan, the amount of interest charge you pay declines while the amount of principal you pay for increases, all while the regular monthly payment remains the same. For our example, the chart listed below highlights how during the course of the loan the interest charge per month would fall while the amount each payment contributes to paying the primary increases if all the month-to-month payments are paid as arranged. How many years can you finance a boat.

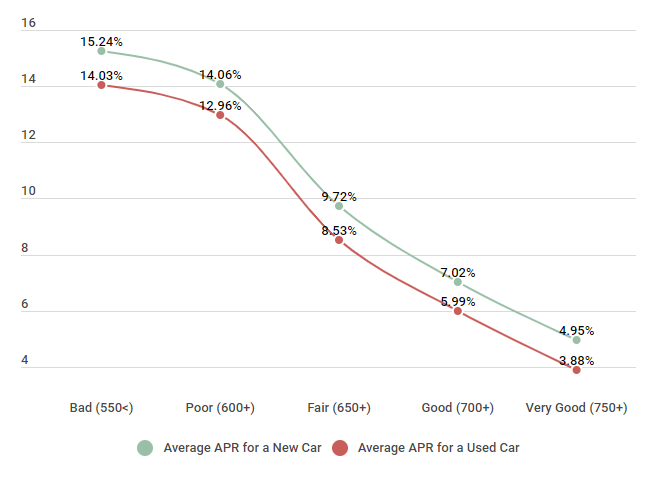

Taking out an auto loan is one of the most typical ways to fund acquiring an automobile. This is specifically real if you are buying a new vehicle, which usually costs too much to spend for in money. Purchasers most typically utilize the aid of a cars and truck timeshare properties loan to cover the greater expense of a new car. A part of this higher expense are the finance charges that loan grantors charge loan applicants for their service and time. You have essentially two ways to figure out the finance charges you have to spend for a vehicle loan, on a regular monthly basis or over the lifetime of the loan.

The very first thing you have to determine is whether you desire to calculate the finance charges yourself or utilize an online calculating tool. Online calculators use an accurate method to determine precisely what you will wind up owing on a vehicle loan, consisting of month-to-month payments. You can find a variety of tool online at different websites, such as Online Loan Calculator. org, Cars. com, and calculators at numerous bank websites, consisting of Bank of America.: By determining the expense of a new auto loan yourself, with all of its associated finance charges and fees, you can make sure that you are getting the finest deal possible.

Frequently, with excellent credit, automobile buyers can get 0-percent APR loans, specifically if they offer a large down payment on the vehicle. First, fill in the numerous fields on the online calculator, such as the lorry purchase cost, any deposit you expect to pay for the automobile, the trade-in value of any vehicle you plan to trade in, interest rate, length of the loan, and sales tax percentage for your state.: Before approaching a dealership about purchasing a car, very first learn what your credit ranking is. This gives you a concept of what you receive and can afford.

Not known Facts About What Are The Two Ways Government Can Finance A Budget Deficit?

You can find your credit history utilizing Experian or Transunion. After you enter your information, press compute. A great calculator must inform you what you can anticipate to pay each month, the variety of payments, the total quantity you can expect to pay, the overall interest paid, and the reward date. Some calculators simplify even further and show you how much you can expect to pay on a yearly basis.: When computing the cost of your new vehicle loan, you typically need to identify the percent of sales tax that you can expect to pay, as well as just how much the title, tags, and other fees will cost in your state.

Pencil and paper Scientific calculator Understanding how much you owe on a new auto loan enables you to understand when you should have your loan settled, in addition to to much better budget plan for other expenses. By determining just how much in financing charges you can expect to pay over the life of the new automobile loan, you can determine if a brand-new cars and truck fits within your long-term budget plan objectives. Some vehicle purchasers choose to determine the monetary charges themselves instead of using an online calculator. Determine your month-to-month payment by utilizing the following formula on your scientific calculator: For instance, a 3 year (36 month) loan of $15,000 at 7% interest exercises to a regular monthly payment of $463.

To obtain the "primary times the rate of interest due per payment" part of the formula, convert the APR to a decimal by dividing it by 100. Take the number obtained and divide it by 12 to get the monthly portion rate as a decimal. Then, multiply the principal by the regular monthly percentage rate. To determine the other half of the equation, get in 1 + the rates of interest due per payment, hitting the button xy on the calculator and entering the variety of payments. Next you would deduct the figure obtained from 1. Divide the first figure acquired by the second figure to get your month-to-month payment.

This need to give you the Overall Quantity of Financing Charges that you can expect to pay.: Make certain to check your work by dividing the quantity you managed the number of payments and comparing that to the overall finance charges monthly. Pencil and paper Scientific calculator In addition to knowing what you owe on a brand-new auto loan overall, having an idea how much you can expect to invest on a monthly basis is helpful as well. Knowing what you owe on a monthly basis enables you to how to get a timeshare better prepare a regular monthly spending plan. Identify your month-to-month payment by utilizing the following formula: To determine the "principal times the interest rate due per payment" part of the equation, you can start by transforming the APR to a decimal by dividing it by 100.

Then, it is simply a matter of increasing the principal by the month-to-month portion rate. Compute the other half of the formula by adding 1 to the the rates of interest due per payment. How long can you finance a camper. Next, hit the xy button on the scientific calculator and go into the number of payments. Then, deduct the figure obtained from the number 1. Divide the very first figure acquired by the 2nd figure to get your overall monthly payment, consisting of financing charges. Next, determine how much principal you need to pay month-to-month. This is as basic as dividing the overall quantity of the loan by the variety of payments.

Rumored Buzz on Which Results Are More Likely For Someone Without Personal Finance Skills? Select Three Options.

To get the principal paid each palm springs timeshare cancellation month, divide the primary amount by the expected payments in months. Last of all, determine the month-to-month finance charges you can anticipate to pay. This includes increasing your monthly payment by the number of payments. Subtract the concept from the number gained to get the overall quantity you owe each month.: You can examine your work by dividing the overall quantity of financing charges by the number of payments. This need to give you a monthly quantity that matches the month-to-month finance charges you computed previously - What does ltm mean in finance. Always make sure that you check your financial scenario by calculating all the associated expenses prior to getting a loan to buy a brand-new cars and truck.